Hi, I’m Sam. I’m on a mission to help women take control of their finances. How? With some simple tips around budgeting, saving and investing.

In this post I’m going to run through 5 things to consider before you deciding between renting vs buying a home.

There are lots of emotional and comfort factors to take into account as well, and these are also important.

I want you to include these financial considerations. Money is an importat factor, plus It’s good to have a sensible framework.

This might be the biggest purchase of your life, after all. Scary, right!

My Story

When I moved in with my partner, we had just moved to South London for work and were planning to stay there for a minimum of five years.

After that, it would be a case of applying for a permanent job. We had absolutely no idea where that would be.

While we were there I was determined that we invested in a property rather than ‘waste’ money on rent.

My logic was that we would likely get a permanent position there because we were familiar with the employers in the area.

So we saved up for the down payment and took out a mortgage on an apartment.

We also spent some money on renovations. We had a housewarming and settled in. It was fun!

Fast forward five years and we wound up getting a permanent job in a completely different location. Yikes!

We had to sell our apartment and lost £30,000 in the process

Some renovations add value to the property but the ones I splashed the cash on didn’t.

So I lost money there too. You’d be surprised at the number of renovations that don’t add monetary value to your home.

To be honest, even if we had stayed in the area we would have had to move anyway.

We were pregnant almost straightaway and needed the extra space. The money would have gone down the drain regardless.

Long story short, buying a home is not always better than renting. sometimes renting is a shrewd financial decision.

So Why Did I Make That Mistake?

Because I had it ingrained in me that buying vs renting was better; I hear so many times

‘it’s better to pay your own mortgage then to pay your landlord’s mortgage’.

I also hear

‘Property is always good investment’.

Sometimes these things are true, but not always.

Below I’m going to outline the key risks you take on when you buy a property.

I’ll also list the risks you hold when you rent a home.

My intention is to give you all the facts, but not to scare you out of your wits!

You won’t get this information from your real estate agent or your mortgage provider.

They are invested in selling you a home. My intention is to make sure that you make the right decision for you.

You might notice that I spend more time on the homeowner risks.

This is simply because I’m assuming that you’re reading this post becasue you’re not a homeowner yet, but thinking of becoming one.

Hence you may be less familiar with homeower risks.

The Key Risks to Consider

Mortgage Risk

A key thing you need to consider when renting vs buying a home is mortgage risk.

Most of us need a mortgage to be able to afford to buy a home, and mortgages are hella expensive.

Not only this, the interest you pay on your mortgage can go up.

What Is Mortgage Interest?

A typical homebuyer’s mortgage is composed of two main things: capital and interest.

- Mortgage capital is the amount you borrowed from the bank to buy your home.

- Mortgage interest is the amount that the bank charges you in exchange for lending you money.

When you pay a monthly mortgage payment you are paying a mixture of mortgage capital and mortgage interest.

The mortgage interest component is a substantial cost, and it is not guaranteed to stay the same over its lifetime.

You might choose a fixed term deal that lasts for 2, 3 or 5 years.

When interest rates climb up and your fixed-rate deal ends, you may find that the deals offered are substantially more expensive than before.

This is because the mortgage interest component of your monthly payment is much higher than before.

In fact, your whole budget can get blown out of the water. This happened to many households after 2022 due to UK Prime Minister Liz Truss’ fateful mini-budget announcement that caused mortgage interest rates to skyrocket.

This announcement was off the back of about 15 years of historically low interest rates.

People had become very complacent and were shocked at the rate hikes.

An Example

E.g. For a home with a £400,000 mortgage

- In 2015 it may have been on a 2.2% interest repayment deal.

- This would have meant monthly mortgage payments of £1,734.

- In 2024 the cheapest mortgage deal it may have found would be a 4.2% interest repayment deal

- This means the monthly payments have shot up to £2,155.

- That is a whopping extra £421 per month to pay the mortgage provider in interest alone!

- That is over £10,000 in interest payments over a two year period.

When you rent, on the other hand, you don’t have to worry about mortgage interest rates. that is your landlord’s concern, not yours. The rent is the maximum price you pay.

But Your Rent Can Go Up Too!

It is absolutely true that when you rent a home you could be faced with regular rent increases, someimes as often as every 6 to 12 months.

But if your landlord tried to jack up your rent by £421 a month like inthe mortgage scenario I highlghted above, you could just hand in your notice and find another place to live.

It’s a lot harder to do that with a mortgaged property.

Maintenance Risk

Another risk to consider when renting vs buying is maintenance risk. If you don’t maintain your property correctly it will not hold its value.

At the extreme, it may even become uninsurable and even un-mortgageable. It may cause problems when you go on to sell the property.

If you buy a flat managed by a service management company, you’ll usually be charged a management fee.

As part of this fee, the company will ensure that the communal parts of your building are maintained and kept up to code for fire and security.

If you don’t have a management company then you are responsible along with your neighbours for doing this yourselves.

In general, you should be budgeting about 1% of the value of your property on maintenance and repairs each year.

This includes the creation of a sinking fund for those big-ticket expenses, some examples are below.

Home Heating

- Your gas boiler will work for about 10-15 years.

- A heat pump will last for about 20+ years.

Windows

- Home windows have an average life span of about 20 years before the seals start to weaken and let the cold in

Kitchens

- Gas cookers last for an average of 20 years

- Good quality white good electrical appliances will last for up to 20 years

- Cheaper models will last up to 10 years

As you can see the list gets scarily long. If you don’t have a reserve of cash to pay for these repairs you could easily tip into debt.

This is a big risk if you don’t have enough financial reserves before making a property purchase.

When you rent however, the landlord takes care of all of this for you. It’s all included in the rent.

So that expression, ‘I’d rather pay my mortgage than the landlord’s mortgage’?

I would change it to:

‘I’d rather pay my mortgage and 1% of property costs for major renovations and repairs than the landlord’s mortgage…. oh and 1% major renovations and repairs, even though the second price is a lot cheaper for me and allows me breathing space to invest more or save for a bigger deposit’

It doesn’t have the same ring to it, but you get my drift : )

Insurance Risk

Another thing to consider when renting vs is the insurance risk.

On 14 June 2017, a devastating fire ripped through a high-rise tower block in West London named Grenfell. 70 people tragically lost their lives.

The source of the fire was found to be an electrical fault in a refrigerator

It was accelerated by a highly combustible eternal cladding that had been placed around the building.

After this tragedy, the UK government launched a major inquiry. One of the outcomes was a full review of all buildings with similar cladding.

While this was played out people who owned apartments in buildings with cladding were unable to sell their apartments until the outcomes of the review and certain approvals have been completed.

People were effectivly trapped in their homes and unable to sell them for years. The rules have only just been relaxed as of 2024.

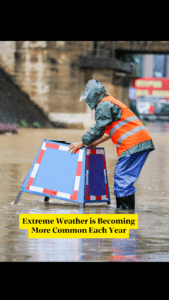

In another example in Florida USA, where several homeowners are facing astronomical rises in their insurance premiums.

This is due to both climate breakdown and many houses built in Florida during a time of poor housing regulation.

The houses have now been found to have many faults and poor resilience to climate breakdown

Record numbers of homeowners are now selling off their homes because they can’t afford the insurance premium hikes.

Climate breakdown is not reversing any time soon, and it is not limited to Florida.

Flooding, storm damage and other extreme weather events are only projected to worsen over the years unfortunately

: (

This will have a knock-on effect on home insurance premiums, and deductible expenses (the amount we pay before the insurance covers the costs) and the general risk to property as an investment.

Renting Has Its Own Risks

Of course, when you rent you also take on risks.

Your landlord could jack up the rent every six months.

They might be unreliable with repairs and maintenance.

They might even ask you to move out with very little notice, even if you’ve been a model tenant for several decades.

You don’t have to face any of these obstacles if you’re homeowner.

These differences between renting and buying sure make buying sound attractive.

Plus there’s nothing more satisfying than staking out your little corner of the world.

You can decorate and renovate it to your heart’s content. You can put roots down, and pass it to your kids.

All the while knowing that one day, when the mortgage is paid off, you’ll be mortgage-free (the dream!).

So with all this in mind here are the 5 things to consider when choosing between renting vs buying.

Renting Vs Buying – the 1st Thing to Consider: How Much of Your Income Will You Spend on Housing?

The first thing you want to consider is affordability.

Will you be able to limit your spending on housing to 28% of your gross income ?

You don’t want to be spending much more than this (before taxes).

This may creep up to 30 or even as high as 31% in high-cost-of-living cities (HCOL) like London, New York, San Francisco and Hong Kong.

In the UK, the mortgage affordability criteria should help make this calculation for you.

This is a calculation that the mortgage broker will make at the time of your application.

You’ll also need to consider things like any career breaks if you aim to have children in the future.

Spending any more than this amount on housing will put undue pressure on your household.

If you think your housing costs will creep beyond this, I would urge you to consider a smaller home, or a cheaper neighbourhood.

If you are able to keep to this threshold and still maintain investments for retirements, savings, and a healthy treats allowance, then you can consider home ownership comfortably within your reach.

Renting Vs Buying – the 2nd Thing to Consider: Have you Saved 20% of the Asking Price?

You might be thinking that 20% is a tall order, especially if you are only putting a 10% deposit down and taking out a 90% mortgage.

I advise that 20% is a good figure to have in mind for the eventual bill you will incur in the first two years of a house move.

This includes:

- The Deposit or Down Payment

- Search Fees

- Legal Bill

- Moving Fees

- Repair Bills – these are the bills they don’t tell you about*

*In my experience there are always big repair bills on a property in the first 1-2 years after you move in.

The previous owners will stop investing in a home once they make that decision to sell up and move.

They’ll keep it looking cosmetically nice so they can make a sale, but under the bonnet, the house will start to deteriorate.

Even if you pay for a full survey, they won’t pick up on everything.

The Boiler’s on the Blink!!!

You may find yourself with a long list of small things breaking off and needing repair.

A leaky tap. The door handles come loose. The electric shower trips out, that sort of thing.

Or you might get unlucky and a big thing that conks out on you.

Or all of the above could happen. If they do, they could sink you if you don’t have a reserve of cash to lean upon.

Many folks will buy homes and then have plans to renovate them, with more costs again.

Then they have zero reserve funds for those emergency repairs.

Add to that the cash you want to spend to decorate and furnish.

You might to make your new place look nice because you’ve been renting for a while. It all costs a lot of cash.

If you don’t have the money saved, you might find yourself getting into debt without even realising it.

For these reasons, I advise you to save a good 20% of the target price of home you are looking for so that you have a decent cushion after you’ve signed on the dotted line.

Renting Vs Buying – the 3rd Thing to Consider: How Long Do You Plan to Live There?

A big difference between renting and buying is the start-up costs.

The upfront costs of buying a home are HUGE.

My advice is to buy only if you plan to stay there for a long time. I mean a decade at a minimum

We ended up moving after five years and we lost money because of it. We also didn’t recoup the money we spent on renovations – double loss.

Ten years is a good minimum time frame because the initial outlay is so high that you want to be there for a long enough time to smooth that cost out.

If you think you only want to stay in a home for a few years, it’s better to keep renting and saving money for a home purchase.

You’ll be able to save a larger deposit for your home and access cheaper mortgage rates.

Plus you’ll avoid the hassle and moving fees twice in one decade.

The only time I would say it is worth it for a shorter time horizon is if you plan on keeping it and turning it into a buy-to-let/rental property.

This can be a great investment. But it would require you to be able to save enough cash to pay for a second deposit.

You also have the opportunity cost. Investing that money into your pension or an investment ISA is a more tax-efficient way to invest, so think carefully before you do this.

Renting Vs Buying -the 4th Thing to Consider: Could You Absorb an Interest Rate Hike?

As I mentioned earlier, a big kicker of unexpected costs are mortgage interest rates hikes.

In 2022 British prime minister Liz Truss announced a raft of economic policies without explaining how she would pay for them.

This caused panic in the financial markets, who then lost their appetite to lend to British consumers.

The knock-on effect of these was that the cost of lending, or interest rates, skyrocketed.

The Affordability Check

When you apply for a mortgage with the mortgage adviser, she is required to perform an affordability check.

Part of this check will include assessing if your personal finances can absorb a noticeable interest rate hike.

While this can seem very restrictive, it’s meant to protect you from losing your home if you can’t keep up with your mortgage payments. It’s not foolproof, however.

For example, they’ll ask if you know of any big life events happening in the near future. But what if you don’t know about a big life event? Or what if the big life event happens in 7 years?

The average mortgage lasts for about 25 years, you need to think about the long haul.

Make Sure you Have Wiggle Room

As of 2024 we are not at the end of the interest rate tunnel.

Some are predicting that interest rates might not peak until 2027 before starting to inch downwards.

The war in Ukraine, gas prices, inflation and other global conditions are all contributors to persisting higher interest rates.

If you are going to take on a huge debt like a mortgage, you will only have certainty on the interest rate for the duration of the ‘fixed rate deal’.

This is usually 2,3 or 5 years. Beyond this you may be paying less, more or the same in interest.

Less Is More

For this reason it is always better to borrow less than the maximum amount you are eligible to borrow.

Give yourself wiggle room so that you an absorb any interest rate hikes down the road.

Your mortgage broker and your estate agent might encourage you to borrow the maximum but remember they are earning a commission.

Biggest is not always the best!

: )

Renting Vs Buying – the 5th & Final Thing to Consider: Can you Afford 1% Annual Maintenance Costs?

If your home costs £400,000, you’ll ideally have £4,000 (1%) set aside as a sinking fund at all times.

Even if you have buildings and contents insurance (and you should have this), you will have deductibles to pay.

Anyway, your insurance doesn’t cover normal wear and tear.

Expect to spend about 0.1% of the value of your home on regular repairs and maintenance each year.

This includes things like gas boiler service, repairs, and garden maintenance.

You may not spend it in one year, but you might spend it all the following year.

So for that £400,000 home, you can expect to budget £333 a month into a sinking fund for home repairs and maintenance.

Upkeep is Important…and Homely

As I mentioned before, it’s important to invest in the general upkeep of your home to keep it in good condition, free of damp and mould, well insulated and in good working order.

It also makes it a more lovable home of course! It always helps to learn some DIY it really keeps the costs down.

If you are not blessed with a silver thumb then checkatrade is a great resource for finding quality assured tradespeople.

In Conclusion

If you don’t meet all of these criteria, it probably means that you aren’t quite ready to buy yet.

But don’t despair! It just means that you have some more saving to do.

Perhaps you could reconsider your budget for housing.

If you have lower cost areas or cities in mind that will be less of a financial burden, now is the time to give them some serious consideration.

Just like a puppy, a property is not just for Christmas, it’s for life.

But Property Values Are Sky Rocketing!

The advice tends to be that you need to get on the property ladder as soon as possible or risk not being able to afford getting on at all.

I totally get it. This is why I would urge you to invest rather than just saving.

The annualised returns in the stock market are 8% adjusted for inflation. I like to use 7% to be super conservative (the only time I’m ever conservative lols).

If you use tax-efficient vehicles like Individual Savings Accounts (ISAs) or Roth IRAs, this is a really savvy way to grow your wealth.

Returns in the stock market are greater than returns in property over the long term.

They’re also less ‘sticky’, which means that you can generally liquidate them a lot easier than you can liquidate (or sell-off) real estate.

They’re also more tax-efficient, depending on the investment vehicle that you use.

If you want to own your own home in the next 15 years, and you’re happy with the freedom and flexibility of renting until that time, investing in funds is even a great way to raise the money for your deposit.

So that’s my guide for 5 things to consider when deciding between renting vs buying. I hope you found it helpful, please share your feedback and questions in the comments.

Good luck on the home-buying journey, you got this!